This article is brought to you in partnership with Cling Systems.

Summary

The bottleneck in batteries is access.

Battery Industry Pulse: weekly roundup.

Welcome back to another edition of my newsletter! - Week 38 2025

EV and BESS sales are growing, and battery innovation keeps progressing.

Labs and factories are testing new chemistries and formats to extend range, cut charge times, improve cycle life, enhance safety, and reduce costs.

That is what drivers, fleets, and BESS customers want.

Automakers still commit to an electric future, and BESS is emerging as a second demand engine as renewables scale. Governments continue to fund plants for climate goals and cleaner transport.

Many suppliers scaled ahead of that promise. When demand came in below early forecasts, the new capacity turned into surplus.

The result is idle inventory.

New and unused cells, modules, and packs sit on pallets. They lose value with time and prices drift down.

This imbalance will not be solved in a single quarter. Announced capacity is largely fixed, and plants need high utilization to cover costs. Even with demand rebound, surplus takes time to clear.

The strange part is that sellers struggle to sell, and buyers struggle to buy. The market is illiquid and opaque.

Producers rarely reach smaller customers, and smaller buyers cannot get a response from producers. Both sides lose time and money, with batteries occasionally becoming stranded assets.

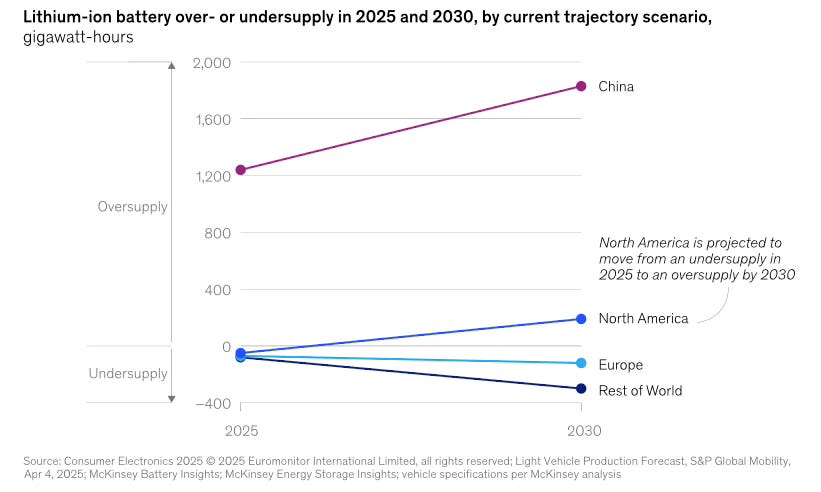

Market overcapacity now and through 2030

McKinsey’s latest forecast model shows the scale of the gap.

Global demand is about 1,970 GWh in 2025 and roughly 3,910 GWh by 2030. Announced nameplate capacity grows faster, to around 6,440 GWh by 2030. Actual output will be lower because of delays and yield loss, but in most scenarios it still lands above demand.

The market is currently in oversupply and will continue through 2030 under all but the strictest supply assumptions. The gap is widest if every announced plant delivers, and while it narrows if only the strongest projects proceed, it rarely disappears.

The regional picture is more nuanced.

China is and will remain in overcapacity through 2030. North America looks tight in 2025 and leans on imports, then swings to surplus by 2030 as new plants qualify. Europe adds capacity but still depends on imports for certain chemistries.

LFP explains much of the pattern. China runs a large LFP surplus. Europe and North America have LFP gaps after prioritizing nickel chemistries early on.

What does this mean for the next five years?

Idle or slow moving stock will remain part of the landscape as programs slip and model cycles change.

The winners on both sides will be the ones that move quickly and build trust.

Sellers who can reach more buyers and clear lots faster. Buyers who can procure surplus and integrate it safely.

In short, the build cycle ran ahead of adoption. The energy transition still needs all the batteries the world can make, and it needs a better way to direct them to the right projects, at the right time.

Sellers: Idle stock loses value without a process

Most idle inventory is new and within spec.

Lots become surplus for simple reasons. A customer iterated a design. A tender slipped. A forecast missed. A plant ran above plan to keep yields stable and teams employed.

Time is the first cost. Calendar aging starts on day one. Even at rest, warm rooms and high state of charge speed the loss of performance. Over months, the SEI (Solid Electrolyte Interphase) grows, electrolytes break down, and internal resistance rises, so power delivery declines. To simplify, the battery degrades over time even when it’s not used.

Price drift is the second cost. Typically, in a buyers market, stock tends to clear at lower prices the longer it sits.

Carrying costs add a third layer as warehousing, climate control, insurance, handling, and risk accumulate. The longer the delay, the more value slips away and more problems for management, treasurers, creditors, and customers.

Large producers focus commercial teams on Off The Shelf (OTS) deals, so they struggle to reach smaller buyers at scale. Surplus lots then end up with brokers, traders, and private threads.

In an opaque market, the process is ad hoc and relationship driven. People swap spreadsheets, PDFs, and messages on WhatsApp or WeChat. Complex B2B deals can stretch beyond one hundred days, which is too long for a depreciating asset.

Real cases show the pattern.

When Romeo Power’s California plant shut, an industrial liquidator listed more than 200,000 new Samsung cells described as ready for use. The inventory, estimated in the tens of millions of dollars, went to auction instead of moving through a structured battery channel. link

ZEVx’s liquidation in Arizona followed a similar path. New LG and Kore Power modules and Zeus packs appeared on a public auction site rather than flowing directly to integrators. The stock was new and unused, yet it did not reach natural buyers quickly. link

A simple process helps.

Buyers deserve a better status quo

Demand exists on the buyer side.

Small and mid sized teams build microgrids, on-site storage, and Commercial and Industrial (C&I) backup. They work with systems in the c5 to 50 MWh range, care about cost and lead time, and need relevant documentation, and predictable performance.

Getting a foot in the door is the challenge.

Tier one producers prioritize multi GWh automotive or integrator contracts with high minimum order quantities and tight terms. New players often lack the operating history and credit to qualify, so they rarely get a slot. That is rational for producers and difficult for everyone else.

As a result, buyers have to turn to informal channels. They work with brokers, scroll private lists and spreadsheets. It can feel like hunting in a fog. Outreach happens on WeChat, WhatsApp, Forums, or LinkedIn, and sometimes through intermediaries.

These paths are slow, uneven, and hard to scale.

Discovery becomes the first wall. Inventory is fragmented, so teams chase several leads to find one lot that fits chemistry, format, voltage requirements, and location. Weeks pass as some leads fade and others change terms.

Often buyers have to deal with sellers who don’t have possession or ownership of the batteries.

Verification forms the second wall. A spec sheet is a pre-requisite and buyers need proof. State of health, internal resistance, open circuit voltage curves, and production dates matter.

So do storage history and traceability. One wrong pallet can erase margin or create a safety incident.

Trust and terms make up the third wall. Many deals have significant gaps between sellers' ask price and buyer bid price. Contract templates vary and sample trades are still being figured out.

The pattern on both sides is consistent. Sellers need faster liquidity with less complexity. Buyers need verified supply with predictable logistics.

Shared infrastructure that standardizes asset valuation, marketing, negotiation, and logistics. The result is shorter cycles, and assets that are optimized for reuse, and eventually recycling.

Introducing S1 by Cling Systems

That shared infrastructure is what Cling Systems provides.

Cling Systems built S1, a product to accelerate battery circularity by improving the process of buying and selling lithium‑ion batteries.

Market access

S1 opens up inventories from verified sellers worldwide. Buyers can filter by voltage, chemistry, condition, and location. Making market exploration for the best reuse, repair, repurposing, or recycling route for each supply possible.Structured deals

Once a match is found, S1 moves negotiation into structured deal rooms, where all requirements are set upfront. Allowing sign-off from finance, legal, management on the seller and the buyer side.Simplified fulfilment

S1 generates shipping documents directly from the deal terms, including the dangerous goods and customs forms. It synchronises sellers, buyers, logistics providers, customs agents, and drivers/captains.Regulation alignment

S1 ensures compliance with the latest battery regulations and standards. Built-in documentation and reporting create audit trails and reduce compliance risk and regulatory delays in cross-border transactions.

Put together, S1 is the digital infrastructure for battery transactions. It brings direct supplier access, structured negotiations, and simplified logistics into one workflow.

For more information, visit Cling’s website or follow on linkedin.

Conclusion: Turn idle stock into active supply

Access is the bottleneck. Factories delivered capacity, policy advanced, and demand reduced, leaving new batteries that are not reaching the projects that need them.

Unlocking that stock means batteries reach their full potential and the circular economy shifts from slide deck to operating model.

Cling Systems and S1 offer one path forward. Use it to turn idle into active and keep the energy transition on time.

Now, let’s look at this week's battery market developments.

Battery Industry Pulse: Weekly Roundup

Metals

Battery

Li Auto and CATL ink new deal to deepen tie-up on battery safety, supercharging tech

China's power battery installation volume in Aug. 2025 jump 32.4% YoY

BESS

EVE Energy's first sodium-ion battery storage system enters commercial operation

BYD unveils world’s largest 14.5 MWh DC energy storage system

Passengers Cars

Commercial Vehicles

BYD unveils e-bus platform with 1,000 volts and CTC technology

Volvo claims a world-first fully electric deconstruction site

📚 Grab the Battery Starter Kit. Use code NEWSLETTER10 for 10% off, exclusive to Battery Chronicle readers.

🤝 For newsletter sponsorships - Click here

🤳 You can also follow me on LinkedIn - Click here

China’s has a no profit motivation in several industries . Lithium ion battery production. Solar Panels. Steel. Aluminum.

They have overbuilt capacity by a conservative 2x in Lithium ion battery production. Steel and solar panels are overbuilt by a conservative 3x.

As you point out, removing middlemen and opening up access to lithium ion batteries to western customers is essential to electrification.

My point is that overcapacity is here to stay for many decades to come.