The European Critical Raw Materials Act: a missed opportunity

Europe’s battery law skips the market incentive. That’s a problem.

Summary

CRMA Cleared the Path. Now It Needs to Push.

Battery Industry Pulse: Weekly Roundup.

Welcome back to another edition of my newsletter! - Week 28 2025

Last year, the European Union passed the Critical Raw Materials Act (CRMA). The idea is to build a battery supply chain that doesn’t rely so heavily on China.

The idea is clear. Europe wants to mine more materials locally, refine them closer to home, and recycle more within its borders. It also wants to avoid being overly dependent on any single country.

But the law has one big flaw. It doesn’t create urgency. The targets are not binding. There are no penalties for falling short. Just goals on paper.

It points the way, but doesn’t force action.

What the CRMA Wants to Achieve

By 2030, the EU wants to:

Extract at least 10% of its raw materials domestically.

Process at least 40% within the EU.

Recycle at least 25% internally.

Source no more than 65% of any material from a single third country.

These apply to key inputs like lithium, cobalt, nickel, graphite, manganese, and rare earths. These materials are critical to EVs, grid-scale batteries, and the broader energy transition.

CRMA sets these as targets, not requirements. There’s no enforcement. No quotas. No import restrictions. Just benchmarks.

It also gives “strategic project” status to certain initiatives. These projects benefit from faster permitting (27 months for mining, 15 months for processing and recycling), plus visibility and access to EU loans and guarantees.

It helps cut red tape. But it doesn’t change the business case.

Where Europe Stands Today

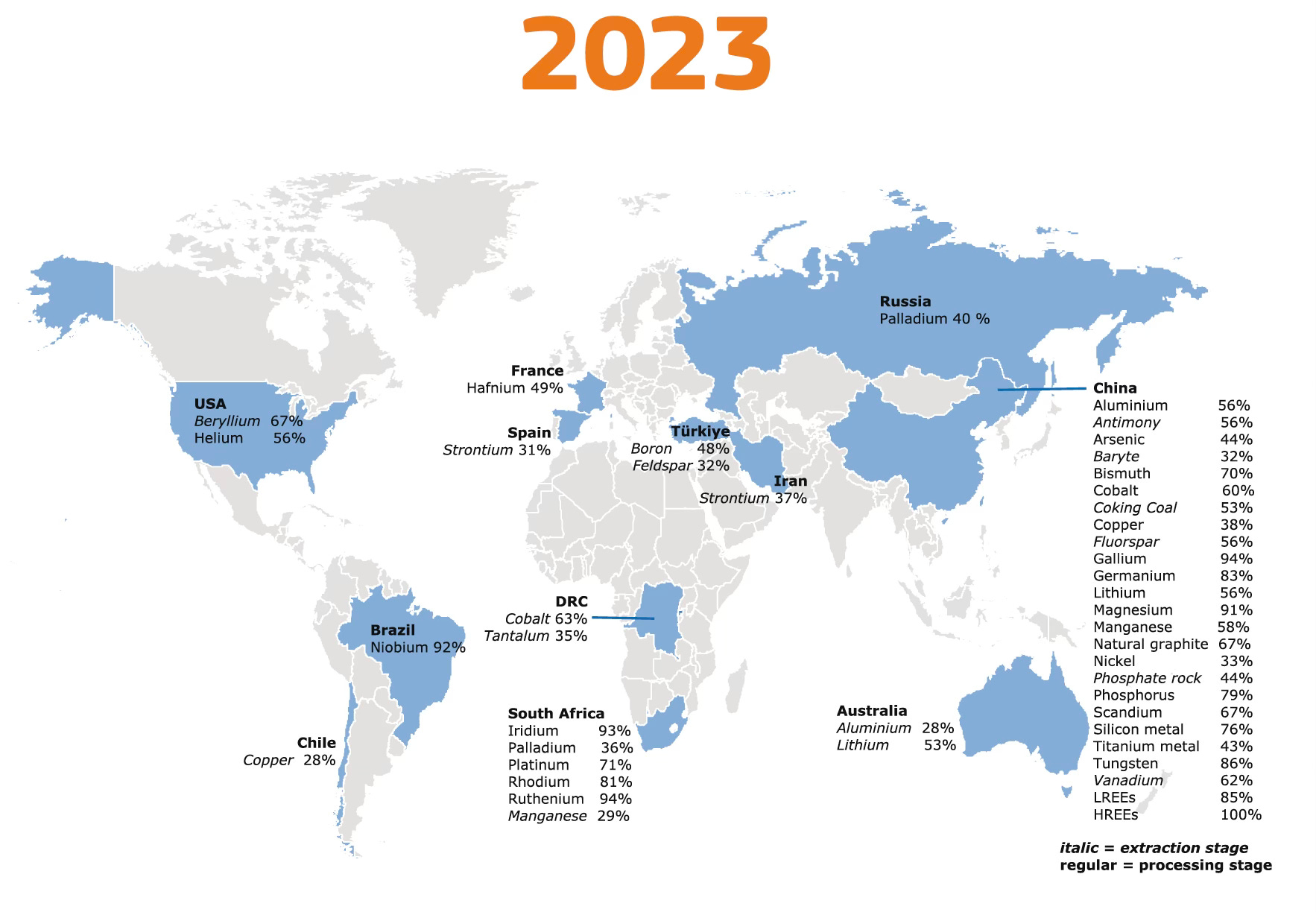

Most of the battery materials are produced in very few countries: China (all the battery materials refining), the DRC (cobalt mining), South Africa (manganese mining), and Australia (lithium mining).

To address this, the EU has approved 47 strategic projects inside Europe and 13 outside. Most focus on lithium mining and refining, graphite, cobalt, and nickel processing, manganese, and battery recycling (lithium, cobalt, nickel).

But many of these projects are still in early stages. Some don’t have financing yet.

Why Some Strategic Projects Are Outside the EU

Not all strategic projects are in Europe. Some are in Canada, Brazil, Zambia and other partner countries.

Why? Because Europe knows it can’t mine and refine everything it needs on its own, at least not by 2030.

These overseas projects reduce reliance on China and help build up friendly supply chains. But they still involve transport, trade risk, and time.

They are useful, but they don’t solve the full problem.

The Core Weakness: No Market Push

CRMA helps, but there’s no pressure to act

If companies meet the targets, that’s good. If they don’t, nothing happens. There are no lost subsidies and no penalties.

That’s the gap.

The U.S. Inflation Reduction Act (IRA) takes a different path. It ties financial support directly to local content. Companies get paid for building and sourcing inside the U.S.

Battery makers can earn up to 35$ per kilowatt-hour in production tax credits (Section 45X).

The IRA doesn’t ask politely. It changes incentives.

CRMA doesn’t do that. It doesn’t say, “Use European-made cathodes or forfeit your support.” It doesn’t reward OEMs or battery producers for local sourcing. And without that, the market won’t change fast.

What Europe Should Do Instead

CRMA opens the door, but doesn’t push anyone through it.

To move faster, Europe should introduce manufacturing credits tied to European content.

If a battery uses European-sourced CAM, anode, or lithium, it should unlock credits: either upstream for the producer or downstream for the OEM or the battery maker.

This would force long-term offtake agreements. It would help early-stage projects raise capital. It would make OEMs build local relationships instead of defaulting to Asia.

Right now, everyone is stuck. OEMs want a secure supply. Suppliers want confirmed demand. Banks want both.

A simple performance-based manufacturing credit would break the stalemate.

Final Take

The CRMA clears the path. It removes some barriers. It puts money on the table.

But it doesn’t change the behavior of buyers, investors, or OEMs.

Europe doesn’t need more goals. It needs market pressure. The IRA created that. CRMA hasn’t yet.

If the EU wants to localize battery supply at scale, it needs to make local content pay. Otherwise, this law will remain a planning tool, not a production driver.

Now, let’s look at this week's battery market developments.

Battery Industry Pulse: Weekly Roundup

Metals

Components

Battery

Panasonic reportedly delays production ramp at US battery factory due to low Tesla demand

SK On Set to Make Inroads into N. America’s LFP Battery Market for ESS

Ford’s LFP Battery Plant Survived Trump’s Anti-EV Blitz. Here’s How

First batch of solid-state batteries from Chery-backed company produced in China

CATL, Geely deepen strategic partnership to accelerate full electrification

Battery equipment

Battery recycling

Passengers Cars

Charging infrastructure

JAC & CATL battery swapping station ready for commercial vehicles across China

Nio has launched its 1,000th highway battery swap station in China

🤝 For newsletter sponsorships - Click here

🤳 I am also present on LinkedIn - Click here