Europe’s battery law has a chemistry problem

The recycling rules still lean nickel-cobalt.

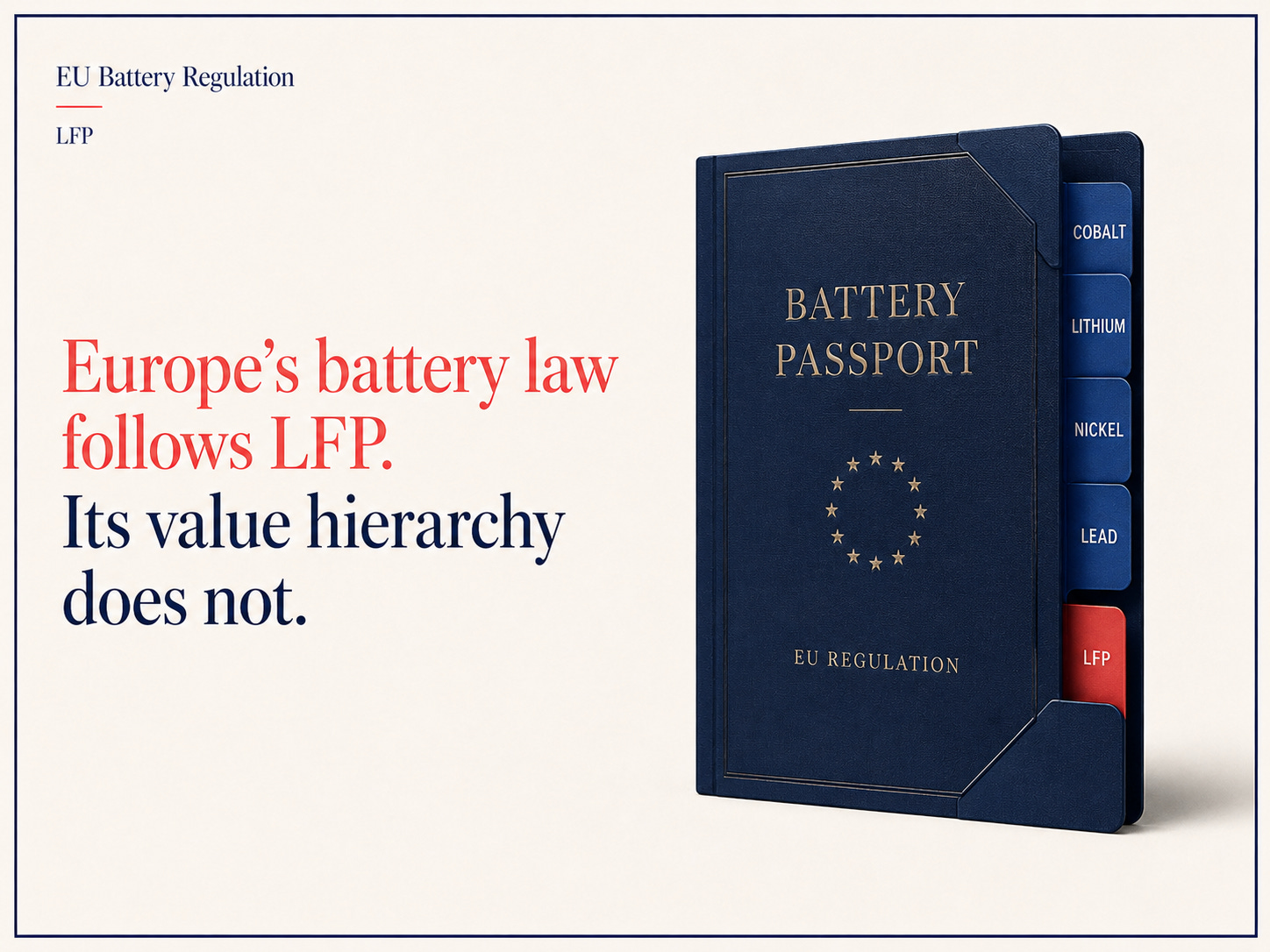

The EU Battery Regulation has a chemistry problem.

LFP is covered, but the issue is what the regulation values.

Lithium iron phosphate batteries still fall under the regulation’s lithium rules, collection duties, Extended Producer Responsibility, due diligence requirements, and battery passport system.

The problem is narrower than that, and more awkward.

The recycled-content part of the law was built around cobalt, lithium, nickel, and lead. That works cleanly for a nickel-rich market. It works less for the market now forming in Europe, where LFP is moving into lower-cost EVs and battery storage.

The law still reaches LFP. But it does not value LFP in the same way it values nickel- and cobalt-based chemistries.

That is where the trouble starts.

What the regulation counts

Regulation (EU) 2023/1542 puts recycled-content targets on four materials: cobalt, lithium, nickel, and lead.

From 18 August 2031, covered batteries must contain:

16% recycled cobalt

6% recycled lithium

6% recycled nickel

85% recycled lead

From 18 August 2036, those targets rise to:

26% recycled cobalt

12% recycled lithium

15% recycled nickel

85% recycled lead

The 2031 targets apply to EV batteries, SLI batteries, and industrial batteries above 2 kWh, except industrial batteries with exclusively external storage.

LMT batteries enter later, with documentation from 2033 and minimum recycled-content thresholds from 2036.

Recyclers also face recovery targets.

By the end of 2027, they must recover 90% of cobalt, copper, nickel, and lead, and 50% of lithium.

By the end of 2031, those targets will rise to 95% for cobalt, copper, nickel, and lead, and 80% for lithium.

The battery passport arrives earlier.

From 18 February 2027, EV batteries, LMT batteries, and industrial batteries above 2 kWh must carry a digital battery passport. Recycled-content data will sit inside that system.

It is a law with a very clear material hierarchy.

Cobalt, nickel, lithium, and lead sit at the center. Iron, phosphate, manganese, and graphite do not.

That choice made more sense when Europe’s battery market looked more nickel-heavy.

It looks less safe now.

The market moved

Europe is not replacing every nickel-rich battery with an LFP battery.

Premium EVs and long-range models will still need NMC and NCA.

Those chemistries offer higher energy density, and automakers will continue using them where range and performance justify the cost.

But the market is splitting.

LFP is becoming the chemistry for cheaper EVs, standard-range models, and stationary storage. It is cheaper, durable, and avoids nickel and cobalt in the cathode.

That shift is no longer theoretical.

CATL’s Debrecen plant in Hungary has been reported as expected to start production around late 2025 or early 2026.

Stellantis and CATL are moving ahead with an LFP plant in Zaragoza, with planned capacity of up to 50 GWh.

Volkswagen’s PowerCo is building a chemistry-flexible battery plant in Valencia, designed to produce cells using chemistries including LFP and NMC.

LG Energy Solution has agreed to supply LFP cells to Renault’s Ampere business from late 2025 through 2030.

The exact chemistry mix will vary by plant and customer. But the direction is plain enough.

Europe’s future battery market will not be a single-chemistry market but segmented.

LFP will take more of the cost-sensitive market. Nickel-rich chemistries will hold the premium end. Battery storage will lean heavily toward LFP.

The regulation was not written for that mix.

LFP is covered, but not rewarded in the same way

An LFP battery still has to comply with the Battery Regulation.

It still faces the lithium recycled-content target. It still falls under collection and treatment rules. It still has to fit into the passport system. Producers still carry responsibility for end-of-life costs.

None of that solves the recycler’s problem.

A nickel-rich battery gives recyclers several valuable metals to recover. Nickel and cobalt help pay for collection, processing, refining, and compliance. Lithium adds more value.

An LFP battery has a thinner revenue stack. It contains lithium, iron, phosphate, graphite, copper, aluminum, and other materials, but the cathode has no nickel or cobalt.

That leaves recyclers with less high-value material to sell.

Lithium can be recovered from LFP. Iron phosphate may also find a route back into new cathode material. Direct recycling could improve the numbers if it reaches commercial scale.

Europe is not there yet.

Until it is, LFP recycling will need one of three things: higher gate fees, lower processing costs, or stronger demand for recovered iron phosphate.

The law can require recovery.

It can make producers pay, but it cannot make bad unit economics disappear.

Graphite is the blind spot

Graphite is still the standard anode material in most lithium-ion batteries. By mass, it is one of the larger active-material streams in the cell.

Natural graphite sits inside the Battery Regulation’s due diligence framework. Article 8 excludes it from the recycled-content targets, and Annex XII provides no recovery rate for it.

That is a strange place to leave it.

Europe has very little domestic anode capacity.

The graphite supply chain is still heavily concentrated in China. Yet the regulation treats graphite differently from cobalt, nickel, and lithium because it carries less value per tonne.

That logic is weak.

A material can be cheap and still be hard to secure.

Graphite should be part of the 2028 review, and Europe needs a recovery plan for it.

August 2026 matters more than it sounds

The next important date is 18 August 2026.

By then, the Commission must adopt the delegated act that sets the method for calculating and verifying recycled content.

That method will decide how strict the chain of custody becomes.

If Brussels allows broad mass-balance accounting, compliance becomes easier. Producers can meet the rule with less direct connection between the recycled material and the battery placed on the market.

That would lower the cost. It would also weaken the link between the regulation and new recycling capacity in Europe.

If Brussels requires tighter physical traceability, the rule becomes harder to meet. More material would need to move through verified recycling and refining routes.

That helps the industrial-policy case. It also adds cost to European cell makers already competing with cheaper Asian supply chains.

This is the real 2026 decision.

The 2031 targets set the destination. The August 2026 methodology decides how companies are allowed to get there.

The law needs to follow the fleet

The Battery Regulation still does useful work. It forces producers to plan for the end of life. It creates traceability. It sets recovery targets. It gives Europe a common rulebook for circular batteries.

But the chemistry mix has moved faster than the law.

The 2028 review should start with the material list. Cobalt, nickel, lithium, and lead made sense as the center of the system when Europe expected a more nickel-heavy fleet. That is no longer the only fleet being built.

Graphite needs a proper recovery plan. Manganese deserves another look. If LFP continues to gain market share, Brussels will also have to decide whether iron and phosphate can remain outside the recovery logic.

The regulation covers LFP.

It just rewards a nickel-and-cobalt battery market more than the one Europe is now building.

That gap is manageable today. By the 2030s, it may not be.

P.S. Whenever you’re ready, here are three ways I can help:

1. Battery industry reports

I’ve published two so far: The Battery Starter Kit, to help you get up to speed on the battery industry, and the CATL Company Profile, to help you understand how CATL operates and why it leads the market.

You can find them here: Battery industry reports

2. Consulting projects

I help companies answer battery-industry questions through a market lens: demand, technology adoption, competitive moves, customer segments, and value chain shifts.

If you’re working through a strategic question, reply to this email with a short note on what you’re trying to figure out.

3. 1:1 paid call

If you have a specific battery market question, I offer paid 1:1 calls when there is a clear topic to work through.

Reply to this email with the question, the context, and what decision you’re trying to make. If it is a fit, I’ll send the next step.

Recycling is complicated.

But learned LFP now getting into more low end EVs; not just large battery storage.